We have all felt that sensation of missing out. You open up some website with the performance results of a system and you see that beautiful upside equity curve which you just wish you could follow. An impulse build inside yourself and self-convincing arguments start to make their home inside your head. You my friend, are convincing yourself to get into a trading system just because you have a fear – and a very human fear – of losing out. On today’s post I am going to be talking about some of the psychological effects of positive performance and why you shouldn’t get carried out by systems that are performing “beautifully”, I will go through the dangers of doing this and I will give you some real life examples of what happens when you approach trading in this way.

If everyone has watched Avatar and thought it was the greatest movie ever then – if you haven’t watched it – you feel like you’re missing out on a positive group experience, you feel an urge to watch Avatar. This very primitive impulse which generates this instinctive fear of being “left out” comes from our distant evolutionary past where those individuals that didn’t care about missing out, missed out on the chance of getting their genes to the next generation. If everyone was talking about how great hunting was across the river and you instead preferred to hunt on your old grounds then your children would have less food and you would have a lesser chance of survival. From an evolutionary perspective there is a very rational justification of why we are all ingrained with the “missing out” fear mark.

–

In today’s world the “missing out” trait isn’t that good as it often generates outcomes that cause losses to those that act on this instinct. A very good example comes from our own field — the financial markets. When everyone from Goldman Sachs to your grandmother seems to be making tons of money buying gold futures it somehow feels that you should get into gold to be “part of the party” however when the latest market participants act on their “missing out” trait they get killed by the markets as the initial players are withdrawing their profits. In commodities, stocks and currencies it works in the exact same way, speculators pile up with the expectation of gains and after the first ones have taken their toll the ones who act on the fear instinct of missing out get the “rough side” of the deal.

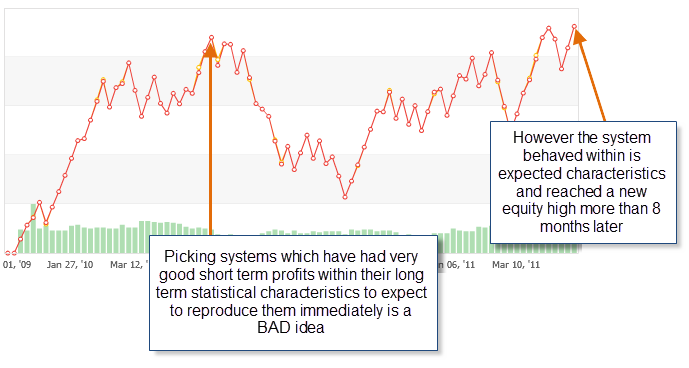

When we examine trading systems we can come to a similar conclusion. Do you have that feeling that a system always tends to go bad the minute you start using it? Is there this impression that you have some sort of “dark cloud” that makes all systems you buy fail? Probably the reason why you start to get this impression with time is because the way in which you pickup systems sets you up for this exact scenario. If you go through 100 trading systems and choose only those that have been able to make 40% profit or more during the past year you will find out that the system will start to lose money just as soon as you load it into your account. This leads you to rotate systems and to believe that there is an inherent back luck to your own trading.

What happens here is that systems follow a direct correlation between the incidence of a draw down period of a certain depth and a straight period of short term returns. A system that has made 50% during the past year with draw downs not exceeding 5% is more likely to get into a deeper draw down than this value than what it was a year ago. Through a careful analysis of many different strategies I arrived at this quite important conclusion which seems apparent when you look at any financial instrument which allows profit from simple carry (profitable buy-and-hold instruments) the steeper the move up, the harder and longer the fall will be. What you get is that systems tend to attract people just as any type of bubble does, the steep, constant and seemingly low-risk return is a tempting and therefore people get into the trap.

When you systematically pick systems for short term steep returns (what most people do) you quickly see that these systems tend to fail harder and give the trader the impression of being “cursed”. Even if the strategy doesn’t even fail according to its long term statistical characteristics but merely goes into what can be considered a “normal” draw down period traders will just feel extremely disappointed that they didn’t get the returns they would have expected to get (those of the short term profitable period they saw). Showing positive short term performance is dangerous because it leads to the disappointment of traders that pick systems in this way, since most people search for short term large gains with low risk it becomes a natural way to disappoint anyone in the medium term.

If you asked me I would say that any time to get into a system is no better than any other as we cannot know the future, but certainly the key is not to enter at any particular period but to be VERY CONSCIOUS about the LONG TERM statistical characteristics of a strategy. If you start to trade a strategy after it has made a 120% profit during last year and you face a 30% draw down which was predicted within the long term statistics then don’t be surprised. As the Asirikuy mantra says you should understand, expect and evaluate your results in the light of long term evidence and formal statistical tests (like Monte Carlo simulations). It is also very important here for you NOT to draw wrong conclusions: the fact that systems that have had strong short term profits have higher probabilities to draw down does NOT imply that systems within long draw down periods are more likely to have short term profits, such a correlation does not seem to exist as systems within long draw downs are just as likely to remain within a draw down or increase their losses. Perhaps the best time to get into a system might be right after a long draw down period ends (which means that the system “still works” and the market “owes it” for all the draw down period length) but this is just a hypothesis right now.

If you would like to learn more about automated trading and how you too can learn how to evaluate and trade systems based on formal statistical analysis (no guessing of when you should stop trading, how deep the expected draw down will be, etc) please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach towards automated trading in general . I hope you enjoyed this article ! :o)

{kind=link}

Hey Daniel, interesting post!

In my opinion I don’t think it is possible to draw any conclusion regarding when to enter a system, because as we see in the monte carlo simulation, there are thousands of scenarios that can be expected, some having no correlation what so ever.

But it makes sense to think that the longer a system was in draw down the better chance it has to start off with a good linear growth pattern, but I won’t base my “pick” on that assumption. I would rather pick a system with a good growth over a year, having some evidence that the system is able to generate profits,rather than choosing a system in draw down with no real life evidence that it is able to generate profits.

Although that is just my opinion in the end I’m still learning all this

Hi Franco,

Thank you for your comment :o) Well as I said on the post I do agree with you but currently have several hypothesis on what might consitute better system entry solutions. Of course there is till no evidence that favors any particular entry strategy and it will be a while before we gather the data necessary to draw conclusions. I do not believe you should pick up strategies that have been losing for a long time but I think that strategies that have been losing for a while and then reach a new equity high offer the best entry opportunities (as I said before a ton of research needs to be done here still). thanks again for posting,

Best Regards,

daniel

PS: The fact that most people would choose systems in such a way (choose a long term profitable system with recent good returns rather than a system which has been within draw down but has the same statistical characteristics) points out to the fact that the notion that entering systems after new equity highs from long draw down periods is a good idea (I have always seen that the “best thing to do” is always the hardest from a psychological perspective). Note that from a statistical perspective both make sense.

Daniel-

Interesting post and it definitely points out the danger of chasing performance.

I try to combat this problem in Forex by entering systems only once a year – typically at the start of the calendar year. All things being equal though, I would rather invest in a system that recently had a new equity high versus a new equity low. This is simply because systems that perform best over time make more new equity highs than equity lows. Looking at the chart above, your arrow shows the worst possible time to enter the system. In reality, you could have entered at any of the new equity highs to the left and still done pretty well by the time the year was out.

I think somewhere implicit in your thinking is that returns are randomly distributed and past performance is absolutely no guarantee of future results. I’m not sure if that is really the case, and I can’t prove it statistically. Maybe i’m confusing stocks with Forex systems.

Anyway, give it some thought and keep the great work!

Chris

http://fx-mon.blogspot.com

Hi Chris,

Thank you for your comment :o) Well you’re definitely right in that I believe performance is no guarantee of future results! However as I said on the post I believe there might be some way to decide on a better entry point than “anytime” for forex systems. This may have to do with a new equity high after a prolonged draw down period but I still have to test this hypothesis (still no evidence that this is a better choice). My experience tells me that whatever you do you should choose systems for their long term statistical characteristics instead of any short term returns, since doing this makes you more psychologically vulnerable as you will be expecting profits in line with the current short term returns. As long as you keep your eye on the long term statistics there is no harm in choosing systems and entering them whenever you want to. Of course a very interesting subject for further investigation :o) Thanks again for posting!

Best regards,

Daniel