To begin my journey in portfolio building with Asirikuy systems I first tried simple combinations of all the systems to see what overall improvements I could achieve within their performance. I will show you today the effect of building a 3 system portfolio from Watukushay No.2, Teyacanani and Watukushay FE which are perhaps some of the most popular systems within Asirikuy. These systems all have a high like hood of long term profitability with 10 year profitable results and a good possibility of being live/back testing consistent. In fact, both Watukushay No.2 and FE have been trading for almost 6 months with consistent results with simulations. Since Teyacanani only has about one month of live trading, consistency cannot be evaluated yet but preliminary results look good.

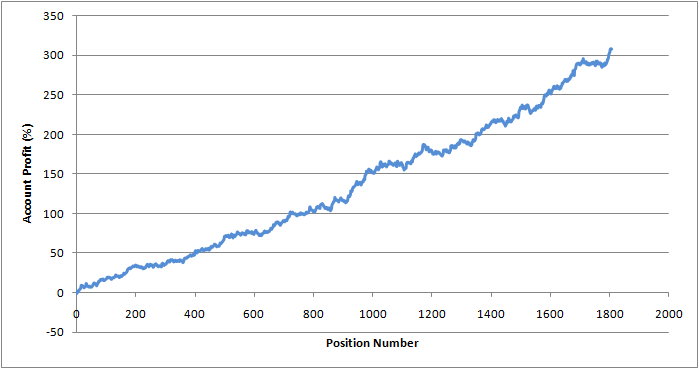

What was the effect of combining these systems ? I have to say that I was impressed by the synergy I got when I joined these trading systems within a portfolio. By using their 10 year – Risk 1 – backtesting results and combining them using the tools developed by two Asirikuy members I was able to easily analyze the results from these three different systems combined. This is inline with what you would get by running the three within a single account since their internal balance mechanism ensures that they only take into account their own profits and loses when calculating their balance. Below you can see the equity curve for this 10 year combined analysis of their results in simulations.

– –

–

After ten years of trading the systems achieve – by working together – an equity gain of about 309% which is equivalent to a yearly compounded profit level of around 19% (see year by year analysis later on). Perhaps the most impressive aspect is not this but the fact that the maximum draw down level of this portfolio combination was very low, at only 5.15%. Not only is the draw down small but it is actually smaller than the draw down level of almost all the systems used. Watukushay No.2 has a maximum draw down of 5.2%, Teyacanani above 6% and Watukushay FE just above 3% showing that the systems are indeed able to reduce draw down to a lower level. Profitability was greatly increased – since the effect of profitability is additive- while draw downs were globally diminished. The overall consequence is the achievement of a yearly profit to maximum draw down ratio of 19:5.15 or 3.68, a wonderful number for any trading system.

An interesting effect also comes when you consider the length of the maximum draw down periods. The maximum draw down length is also greatly reduced when compared with individual systems. For example, Watukushay No.2 has a maximum draw down length of 259 days, while the combined portfolio has a value of 216 days, showing a diminishment in the duration of the maximum draw down length. This means that not only does this portfolio achieve lower worst-case equity loses but the overall length of these losing periods is reduced.

– –

–

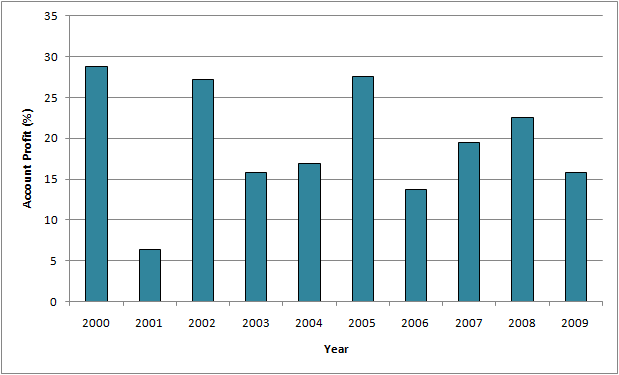

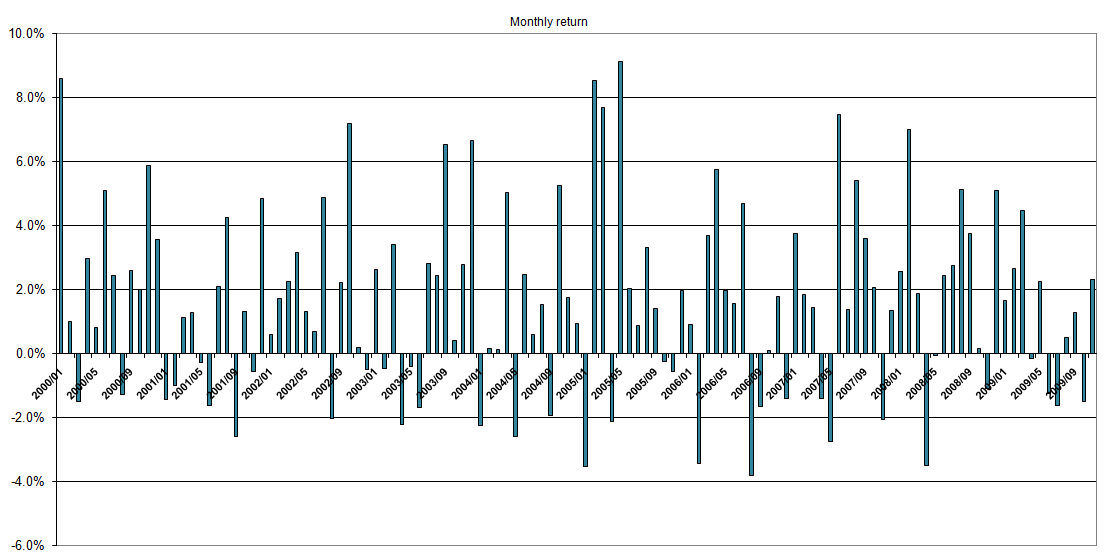

It is also interesting to analyze the yearly and monthly performance of the portfolio to see how it compares with the Asirikuy systems by themselves, something which would show us the arrange of possibilities we could expect for our first year, month and subsequent years of trading this combined system portfolio. The results are shown on the images above and below.

– –

–

The images above confirm that the portfolio is a great improvement when compared with the three systems traded by themselves. Overall, we do not get any losing years for the past 10 years and – even though the draw down of the worst losing months does increase – it does so in a much smaller proportion than the most profitable months. The profitability over the years also increases very significantly showing us that the effect of profits is indeed additive while the effect of combined draw downs is “hedging” in the sense that when any of the systems enters a draw down period some of the others are bound to enter profitable periods. The draw down periods of the systems never overlapped perfectly during the last ten years and only a few months of combined draw down are ever seen. As you see above, the largest losing month does not give us even half the profit of the most profitable month and profitable months are overall much more abundant than losing months.

The significance and analysis of this findings is tremedous. The building of these portfolios will allow us to reach higher profit targets with diminished risk and to have worst-case scenarios (double the projected maximum draw down) that are below our profit targets. This could mean that this same porftolio traded with a Risk = 3 would have an average yearly profit near 57% with a maximum draw down near 15.6% and a worst case scenario of about 32%. The use of portfolio trading will become our most important trading tool within Asirikuy and within the next few months several portfolio live accounts both owned by myself and challenge accounts will hopefully be added to Asirikuy.

I am also building a wealth development plan based on combinations of Asirikuy systems (including all systems and different currency pairs) that will be our final test of all these likely long term profitable systems. A plan with regular additions and a 1000 USD initial investment to get to a 5 figure yearly income within 10 years with a worst case scenario below 50% is what I currently have in mind. As you see I am very excited about these developments as the combination of long term profitable systems is proving to be much more than the simple sum of its parts. I hope you are excited as well so feel free to leave any comments, questions or opinions you may have :o).

If you would like to learn more about Asirikuy systems and to begin your journey towards long term profitability in forex trading please consider buying my ebook on automated trading or joining Asirikuy to receive all ebook purchase benefits, weekly updates, check the live accounts I am running with several expert advisors and get in the road towards long term success in the forex market using automated trading systems. I hope you enjoyed the article !

Daniel,

Are you developing portfolios with NFA compatibility in mind? To my mind, it's of great importance since you can count on those brokers in a larger degree than on those, who arent NFA compliant.

Thanks a lot for all your analysis and effort!

Maxim

Hello Maxim,

Thank you for your comment :o) That certainly raises an interesting problem since all the portfolios I have analyzed up until now would have hedge problems with NFA brokers due to the fact that some systems may have short and long positions opened at the same time. FIFO would also be a problem in this sense since a system may quit a trade before another, even if the trade was opened later.

For people who wish to use the portfolios on NFA brokers each expert would need to be run on a separate account. In the end, the addition of the performance of all the accounts would give us the same results. However this would of course multiply initial capital requirements since several accounts would need to be funded first. However yearly additions would still be done without problems since money can be divided and assigned accurately to each separate system.

Of course, NFA regulations hinder the use of portfolio trading on the same account by a huge extent since they inevitably bring several problems to the opening and closing of positions.

However there are many trust-worthy non-NFA regulated brokers like Forex.com UK and Alpari UK who offer you strong regulation coupled with the liberty to trade as you please. Such a broker would be ideal for the trading of Asirikuy portfolios :o)

I hope this answers the question. Thank you very much again for your comment ! I am glad I can help :o)

Best Regards,

Daniel Fernandez

Hello Daniel,

Could trading different instruments with different EAs solve the issue?

Maxim

Are these EAs publicly available?

Hello Everyone,

@Maxim : It could solve part of the problem but the fact remains that having several systems based on one instrument will probably be necessary. This idea would limit you to one system per instrument, a fact that will also greatly limit your ability to trade. Having several accounts seems like a better idea overall for NFA brokers.

@Laetitia : Only Watukushay FE is freely available at watukushayfe.blogspot.com, the other systems are available for a very small price at http://www.asirikuy.com.

Thank you very much for your comments :o)

Best Regards,

Daniel