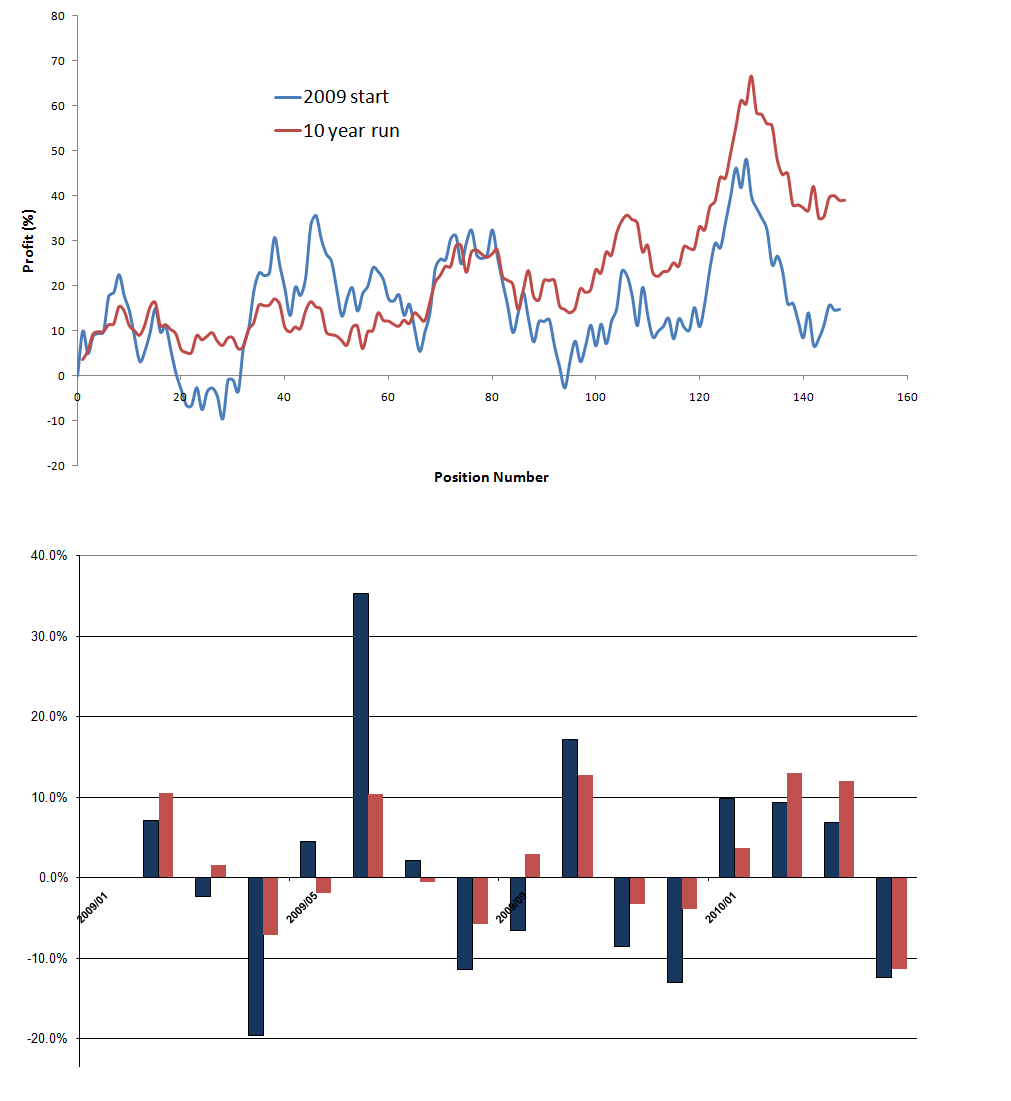

In order to answer these questions I looked at an account started right before a very significant draw down period of the GBP/USD instance which started in mid 2009. I ran a test from January 2009 until May 2010 and compared the results obtained for the 10 year portfolio for these same months. The first thing we can take into account is the draw down figures of both tests. The maximum draw down in 2009 of the 10 year test was near 9% while the maximum draw down for the test from 2009 to 2010 is 28%. It is however worth noting that this 28% is inline with the maximum historical draw down of the 10 year portfolio which is 30%. Looking at the equity curves of both systems displaying percentage gains and looking at monthly performance gives us a better idea of what is going on.

– –

–

As you can see, the 10 year portfolio has already diminished the participation of the GBP/USD instance significantly while the 1 year and a half test still has both experts contributing roughly the same since they haven’t had a chance to compound profits significantly. The result is that the strong draw down period on the GBP/USD eliminates a lot of the profit of the EUR/USD instance but the profit made by the later is enough to hedge the loses made by the GBP/USD account and put the overall portfolio in a profitable point.

I have to say that a careful analysis of similar periods – in which an account is started right before the worst draw down case of the worst performing instance – reveals that this is exactly when the maximum draw down portfolio levels are reached. In this case, a level of about 28% was reached which is close to the expected maximum historical draw down of the ten year portfolio (starting in 2000) at 30%. Running different initial periods were the account is started right before a GBP/USD instance unfavorable period shows us that draw down between 20-30% show almost all the time. However, the EUR/USD instance is always able to hedge this draw down and get the account to the other side.

As we saw on part number one of this article, the overall larger compounding effect of the EUR/USD instance ends up eliminating most contributions of the GBP/USD instance as it fails to perform up to the same level. Interestingly, this shows that the startup point does not increase risk but the 10 year maximum draw down appears to be the draw down combinatorial “upper-limit” that determines the draw down attained when experts are started within an unfavorable period. The 10 year estimation therefore becomes a valid estimate of future draw down limits and doubling it provides and accurate worst-case scenario.

In the case of systems with very different performance levels, the use of a continuous portfolio in which the most profitable systems take lead seems to be a good solution. However it is still easy to wonder if there is any other better way. Is there a better way when systems have similar profit levels ? Is there a way of examining portfolios in which we can be absolutely sure that the importance of the startup point is not critical ? How can we trade a portfolio in such a way that a very clear draw down limit is attained ? Answering all these questions and studying portfolios in depth has led me to the development of a series of portfolio guidelines and investment rules that I will talk about on tomorrow’s post and that will be discussed in depth this Sunday on an Asirikuy video… Stay tuned for the release of the Atinalla project.

If you would like to learn more about my journey in automated trading and how you too can develop a portfolio of likely long term profitable systems based on sound trading tactics please consider buying my ebook on automated trading or joining Asirikuy to receive all ebook purchase benefits, weekly updates, check the live accounts I am running with several expert advisors and get in the road towards long term success in the forex market using automated trading systems. I hope you enjoyed the article !

Hello Daniel,

The problem is that it is impossible to know that the day of starting the portfolio is a beginning of a worst draw down case. We will know it much later: during the past performance analysis. Have you dealt with this issue?

Maxim

Hello Maxim,

Thank you for your comment :o) Indeed, what you say is entirely true. The intention of my analysis is not to predict whether or not we will be going into a worst draw down case but to give us an idea of what the effect of such a case would be.

You will see that there are much better ways of handling a portfolio, having much better control over overall draw down conditions. Thanks again for your comment :o)

Best Regards,

Daniel