I believe that this is the story that goes around time and time again and what causes the general perception that “higher trading frequency” is better because it achieves faster profitability. In reality it doesn’t necessarily do this but it only ensures that there is a faster turn out of the system’s character and increases the number of trades per draw down and profitable period. So with a system that trades very often (5-10 times per week) you may get a lot of profit very quickly when the market is favorable and then when the market exposure is cashed you will get a lot of loses.

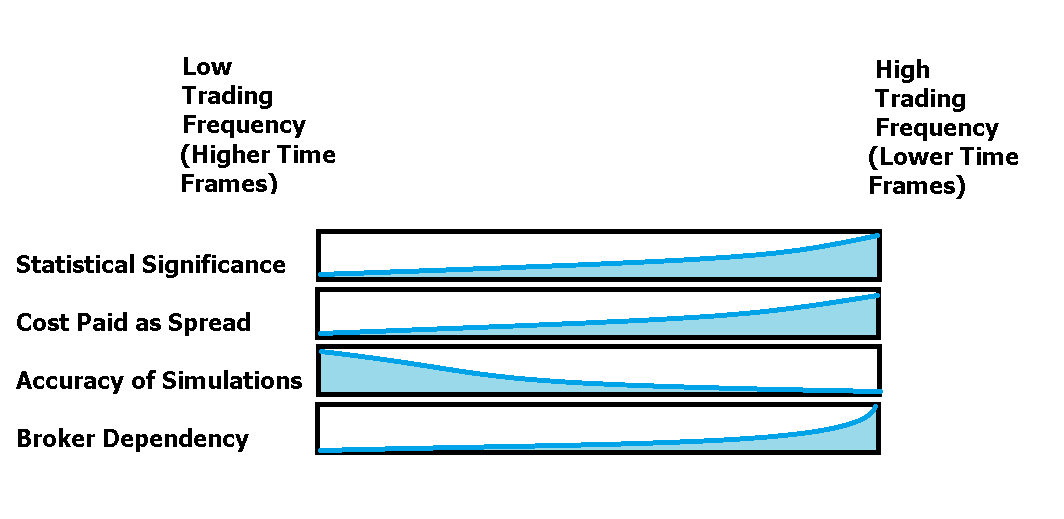

To be clear here, the trading frequency of a system is only an aspect secondary to the system’s profitable character. You can have a system trading twice a year achieving the same profitability as a system that trades 10 times a week with some differences that make the first choice better. The most important thing here is the accuracy of the measurement of profitability. Generally systems that trade very often trade lower time frames and lend themselves to further broker dependency and inaccurate simulations while infrequent systems trading higher time frames will give very accurate and broker independent simulations that will allow you to have MUCH better estimates of profitability.

It is also true that the “effort” a trading logic needs to do to come out with profit if it trades frequently is much higher because it needs to make up much more money in spreads. A system that trades an average of 10 times per year pays only 10 times the spread while a system that trades 200 times each year pays 20 times more.

– –

–

The fact is that the only advantage that frequent trading systems have over infrequent ones is the actual statistical significance of the simulations which is higher for a frequently trading system (if the simulations are indeed accurate). So a system that trades only once each year will have only 10 trades for the past ten years (which could not be interpreted as being long term profitable or unprofitable due to the small size of the sample) while a system that trades 100 times each year has more than 1000 trades which are more than enough to establish long term profitability – again – given accurate simulations.

However the advantages we get when we lean towards systems that trade infrequently is higher since we have an overall reduction in trading costs plus a gained accuracy in simulations which are vital to address the profit and risk targets of our different trading systems. For this reason the best compromise between both worlds seem to be systems that average 1-1.5 weeks every week with about 50-75 trades per year. These systems are generally traded on the one hour charts although use of higher time frames would also encourage less broker dependency and higher reliability. For example, the Ayotl trading system – my implementation of the turtle trading system – trades on the daily time frames with about 10-20 trades per year, giving very accurate simulations and a general lack of broker dependency. Systems like Watukushay No.2 trade much more frequently but this comes at the cost of higher broker dependency and spread costs due to the lower time frame used (one hour).

So as you see, more trading doesn’t mean better since when this is taken to extremes simulation quality is drastically reduces – to the point of being pointless – and spread costs become a dramatic part of your trading system’s profitability. If you would like to learn more about automated trading systems, their characteristics and development please consider buying my ebook on automated trading or joining Asirikuy to receive all ebook purchase benefits, weekly updates, check the live accounts I am running with several expert advisors and get in the road towards long term success in the forex market using automated trading systems. I hope you enjoyed the article !

hi daniel,

that's a very good article. i agree with you about the topic. but i think a system that trade less than 20 times per year is very dangerous because it's profitable often depend on few trades. I prefer a system that make at least 50 trades per year, where in the simulation i use a spread 1,5 time wider than normal spread in the pair.

thank for you articles.

andrea

Hi Andrea,

Thank you for your comment :o) Indeed, systems that trade infrequently have the problem of being sensitive to execution problems. For example, many of these systems base their yearly profitability on 2-3 trades each year so missing out on one of these opportunities due to any eventual problem could be effectively devastating to performance. For this reason I agree with you in using systems that trade an average of 50-70 times per year. This is indeed a balance between the advantages of long and short term systems.

However you have to take into account that the spread is not the only factor affecting a system which trades very frequently, inaccurate simulations due to very small timeframes or inadequate coding may also cause large broker dependency and lack of reliability in the projected profit and draw down figures. However whether or not these factors are an issue depends on each particular system.

Thank you very much again for your comment :o)

Best Regards,

Daniel