–

–

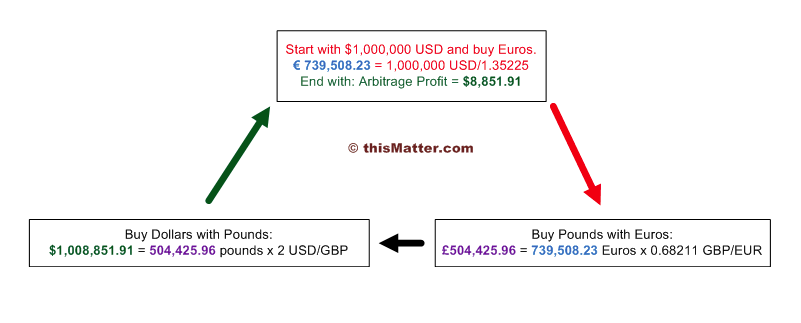

–The three way arbitrate inefficiency now arises when we consider a case in which the EUR/JPY exchange rate is NOT equivalent to the EUR/USD/USD/JPY case so there must be something going on in the market that is causing a temporary inconsistency. If this inconsistency becomes large enough one can enter trades on the cross and the other pairs in opposite directions so that the discrepancy is corrected. Let us consider the following example :

EUR/JPY = 107.86

EUR/USD = 1.2713

USD/JPY = 84.75

The exchange rate inferred from the above would be 1.2713*84.75 which would be 107.74 and the actual rate is 107.86. What we can do now is short the EUR/JPY and go long EUR/USD and USD/JPY until the correlation is reestablished. Sounds easy, right ? The fact is that there are many important problems that make the exploitation of this three way arbitrage almost impossible.

The first problem is the trading cost. This three way arbitrage is based on taking very small profits from the market and as such it becomes extremely vulnerable to spread variations. A bad spread means that you will lose most of the profitability or that you will need to search for very large arbitrage gaps which are rare and often fall in line with news events when trading spreads are much higher and trading becomes much harder.

The second and biggest problem is execution. Not only will it be extremely hard to get into these orders without any slippage (since your profitability depends on it) but getting out might be even harder as you will be trying to squeeze a very small amount of profit from the market. These arbitrage opportunities are also searched by funds with ultra fast computers and direct connections to banking feeds and therefore the liquidity related to them will dry up terribly fast.

The simple fact when trying to trade three way arbitrage is that for a retail trader it will be almost impossible to profit given the amount of trading cost, the rarity of very good opportunities and the speed in which these opportunities “dry up” as traders with access to much faster computing power take advantage of them. In the end trying to exploit one of these trading techniques is bound to be MUCH harder than trading a simple long term profitable system since their profitability will depend on too many factors which the regular retail trader cannot control. As a matter of fact, the exploitation of every arbitrage opportunity greater than trading costs is something that banks and hedge funds do constantly, a practice that aids to keep exchange rates equalized also making these opportunities for retail traders practically nonexistent.

As always there is no “free lunch” in forex trading and success comes from knowledge and understanding and not from the exploitation of some “magical” trading system that no one else takes advantage of.

If you would like to gain an education around automated trading and learn how you too can make up your own systems with sound profit and draw down targets please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach to trading systems. I hope you enjoyed this article ! :o)