–

–

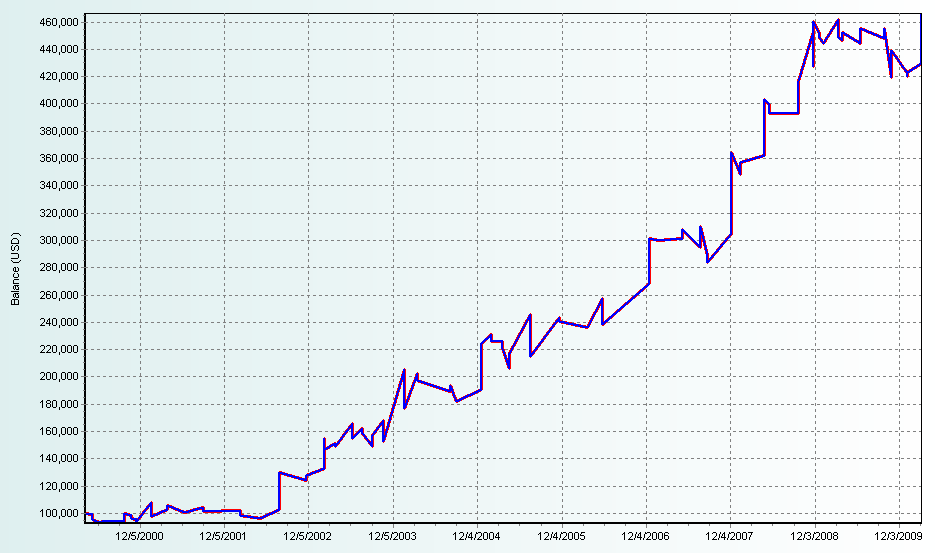

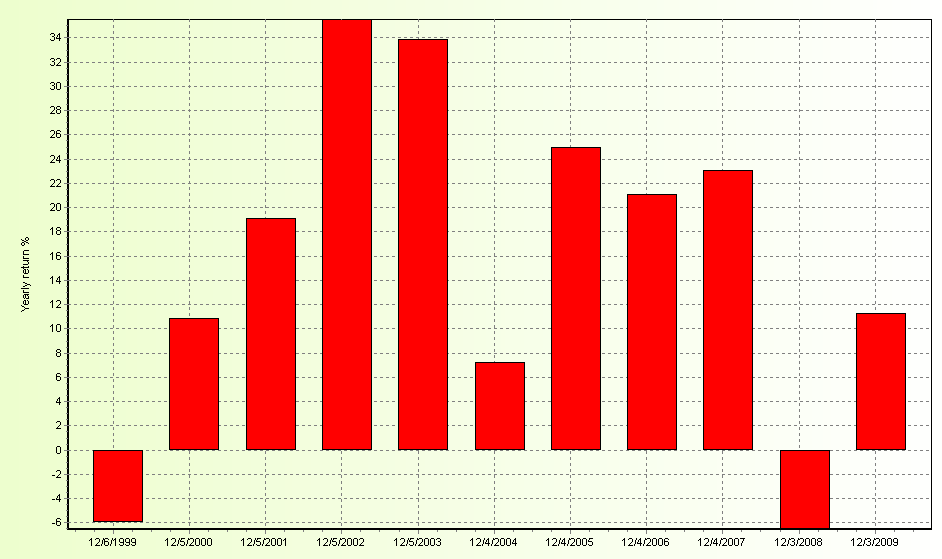

–So does the strategy achieve profit ? The above graph shows you the performance from January 05 2000 to June 05 2010. As you can see the system achieved profits quite consistently over the past ten years, capturing almost every major trend that developed on the EUR/USD during this whole trading period. The system took 170 positions during the past 10 years, averaging about 2 positions every three months. The average compounded yearly profit of the system is 15.85% and the standard deviation of the yearly profits is 13.41%. The best year during the test gave a profit of 35.51% while the worst one was -6.94%.

–

–

–The draw down characteristics of the strategy are also very important to discuss with a maximum historical draw down of 13.81% and a maximum draw down period length equal to 554 days with an average draw down and draw down period length of 8.15% and 242 days. This gives the system a pain index value of 4.92 meaning that it will be easier to trade than the Turtle Trading system from a psychological stand point given the fact that its draw down characteristics are easier to handle.

–

–

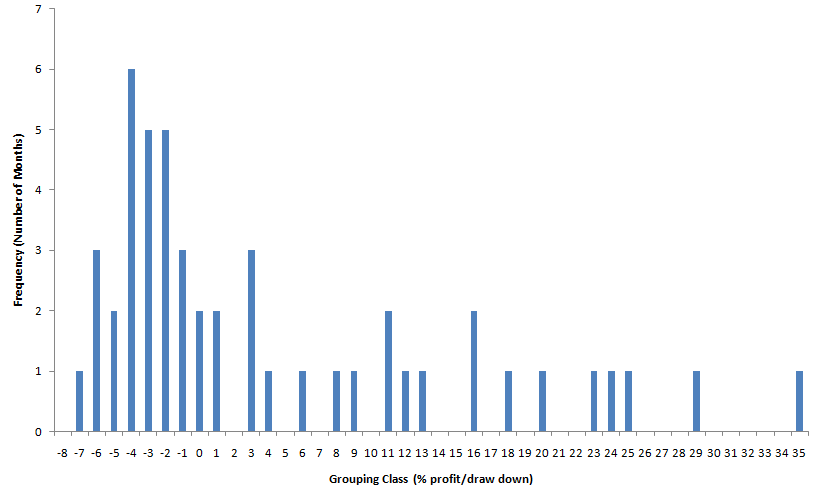

–Another very important aspect to evaluate is the distribution of monthly returns which is shown above. Months were divided into classes grouping months within a 1% profit/draw down range ((-8)-(-7)%…. 1-2%, etc) giving the final distribution shown. This analysis gives us invaluable information about the system which will help us understand how the system trades and what we can expect from it. We can see that the system took trades through only 48 of the 120 months of the test and that the probability of one of those months to come out as a winner was 45% while the probability to have losing month was higher, at 55%. However the losing months were much smaller than the winning months with the average winning month being 11.7% while the average losing month loses only -3.7%. This reflects the risk to reward ratio of this system which along the ten year testing period was a little bit above 1:3.

So what we have here is a system that will only give you trades for about 50% of the months in which you trade it, there is a higher probability that one of those months will come out as a loser but any winning month you may have will be in average three times higher than your average losing month. This behavior is classic of daily trend following systems that aim to profit from long term trends that develop on the forex market.

After this analysis I think that there are simply no excuses. The above is the first manual system – to the best of my knowledge – which only requires 5 minutes to trade everyday, is offered absolutely for free and has a full 10 year historical analysis showing you exactly what you can expect and how your performance is likely going to be in the longer term. Sure, it won’t be easy to trade and you are bound to have a few losing years within a ten year period but the system will allow you to develop your trading skills and most importantly your discipline and your ability to execute a trading plan. Finally trading this will become even easier during the following months as an indicator I developed for this system will be shared in a magazine I’ll be writing for from October… Stay tuned to find out more !

– –

–

If you would like to learn more about other trading systems and how you too can design and trade your own mechanical trading systems knowing exactly what the average compounded yearly profit and maximum draw down figures are please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach automated trading in general . I hope you enjoyed this article ! :o)

hi Daniel,

thanks for the system and yours shared researchs. i coded this system in tradestation and test it on 2001-2010. my results is quite similar to your. but, i have a question about a calculation of lot size. what do you used for contract size? and why don't you used AccountBalance/(2*ATR(30)/ContSize). the initial stop loss is 2*ATR(30), so the initial risk is two time the ATR.

andrea

Hi Andrea,

Thank you very much for your comment :o) The contract size is used due to the fact that the lot size needs to be adapted to different account types. Some accounts have lot sizes of only 10K per standard lot (1 pip in EUR/USD equals 1 instead of 10 dollars) so you need to take into account the contract size to accurately calculate the lots for all accounts.

Regarding the equation. Well, it needs to be expressed this way since with your equation you would obtain exceedingly large values (since you are not multiplying by a 0.01 factor in the beginning, meaning that you are risking the whole account balance on every trade, if you are using absolute ATR values (like 0.0120)). However it is just a matter of expression. You can think of the equation proposed :

0.01*AccountBalance/(ATR*ContractSize)

as equivalent to :

0.02*AccountBalance/(2*ATR*ContractSize)

Meaning that there is a 2% inherent risk per trade. I hope this answers your question. Thank you very much again for your comment,

Best Regards,

Daniel Fernandez

Dear Daniel,

This system is what I have been looking for. I am drawn to the Turtle method, but I appreciate the reduction in drawdown that your system demonstrates.

Do you have any more information / have you produced an indicator for this that could be used.

I am struggling to make forex work as an income generator and any help in operating a good system would be greatly appreciated,

Kind regards,

Giles

Hi Giles,

Thanks for writing. The rules are located in the first part of this post series (here). However using this system would still imply long periods of drawdown – even in the order of 2 to 5 years – so I advice you perform a long term back-test of this strategy before you ever commit to trade it live (otherwise you simply won’t withstand the psychological pressure of a few years under water). I hope this answers your question,

Best Regards,

Daniel