There are many articles out there that talk about the use of alternative money management techniques in order to improve the results of a trading strategy. All of these articles evaluate particular strategies, focusing on the improvement of individual equity curve characteristics as a way to justify the use of a different money management approach. However, these articles neglect to evaluate the overall effect of the new money management technique when taking into account the inherent randomness in the short term distribution of returns inherent to trading strategies, also failing to evaluate what happens when the statistical characteristics of the system change. Through today’s post I want to share some of my analysis pertaining to game theory and equity curve average money management when evaluated through Monte Carlo simulations. This analysis provides us with a deep understanding about the effect of these money management techniques as well as why we might use or avoid using them within our trading configurations.

First of all it is important to discuss our definition of money management for this article. A money management technique – as we will be discussing within this post – is the tactic used to decide whether a trading strategy should be traded or not and how much money a strategy should risk. In essence the money management encompasses both the decision to allow or not allow trading and how much money is risked if trading is indeed allowed. In the case of a regular system – basic money management – a strategy is always traded and risk is proportional to the account’s balance (being a percentage of this value per trade). On the advanced money management cases – game theory and equity curve average – a decision is made to stop trading whenever a system’s historical results have reached certain conditions, in both cases a parallel “ghost” trade history is kept to make these decisions (in the ghost history all trades are taken). In the equity curve average case trading is stopped whenever equity is below the average of the past 20 equity values while in the game theory case a score is given to a strategy based on its previous profitable/losing trades and trade/no-trade decisions are made based on a random number roll and its relationship to this score (the higher the score the more likely we are to trade and vice versa). When trading, both of these strategies also risk a percentage of the account balance, as the regular MM — this is the case to avoid lot size granularity issues.

–

–

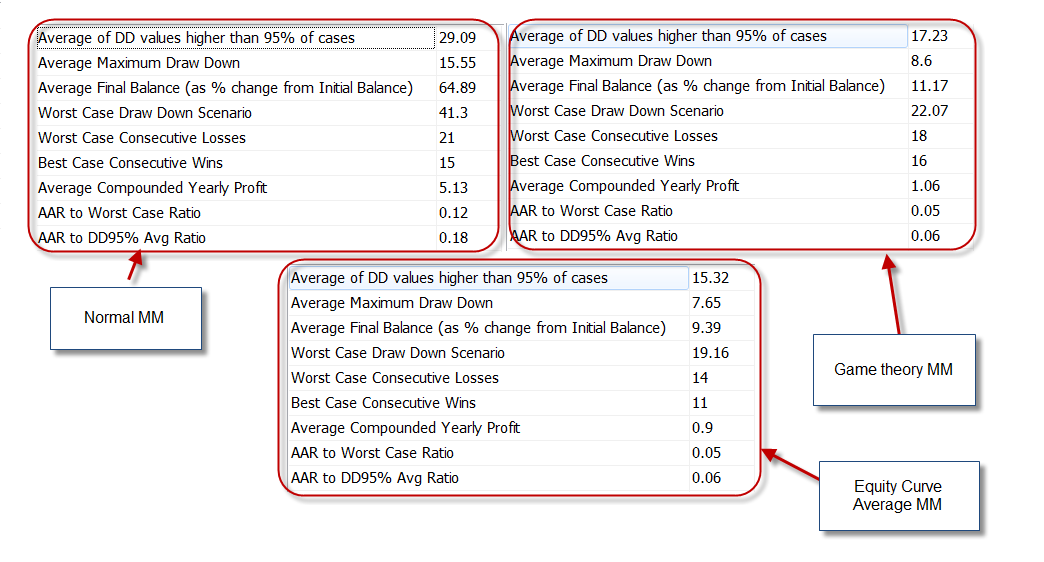

To evaluate how these two MM techniques work in comparison with our regular MM we need to run Monte Carlo simulations of the strategy using the three MM techniques, comparing differences that may arise in the results. The results showed here were obtained with 100K iterations (400 trades per iteration) using the distribution of returns of a typical trading strategy. First of all we need to evaluate how the advanced money management techniques change the overall results of the simulation when the strategy doesn’t change (when it behaves as expected). As we would expect the worst case scenario and the final average profits are both reduced due to the fact that the advanced money management techniques make us miss trades (trade less) and therefore we are not seeing as much trading as with the regular simulation. Overall we see that the average profit to worst case drawdown value drops to about one third of the value with regular money management. Expanding the number of trades to higher values reveals similar results with the worst case drawdown scenario eventually converging with the value for the normal simulation and the AAR to drawdown ratio dropping to about one third to one fifth of the original value.

The above shows us something to be expected, if a system behaves exactly as it should the advanced money management techniques will always generate an equal or worse result. If a system behaves as expected the long term worst case scenario for all money management techniques remains the same, this is because the worst case scenario is a property of the distribution of returns of a trading strategy; it doesn’t depend on the money management you use (provided that risk per trade remains unchanged). This means that if you’re using one of these money management techniques and the system works exactly as you expected – future statistical characteristics equal or better than historical results – you will regret your decision to use this money management as you will be missing a significant portion of the profits you would have otherwise achieved. In other words, you are sacrificing potential profits by being too careful; you’re paying insurance.

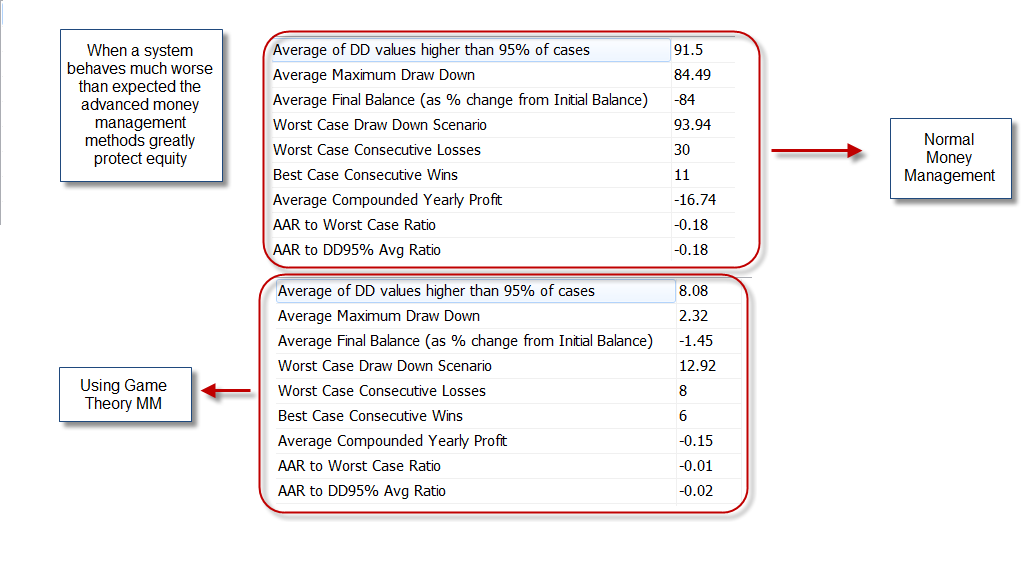

So why would anyone use these MM techniques if results are worse than with normal MM ? The answer comes when we study what happens when the systems do not behave as we expected. When a system’s statistical characteristics are worse than what we expected historically – the distribution of returns is in reality much worse – the advanced money management techniques do us the great favour of protecting us against this. The results below show – quite dramatically – how the game theory money management compares with the regular money management when there are negative distortions present in the distribution of returns (it is far worse than expected). As you can see, when the distribution of returns is skewed towards losing territory the advanced money management protects us very well. While the average final balance for the game theory portfolio is -1.25%, the average final balance for the normal money management is -84%. This means that if you were trading both of these techniques you would have been able to exit this period with a maximum drawdown of 12.9% when using game theory (with a very good chance of exiting with only 1-2% drawdown), while with the normal MM you would have exited at the MC worst case scenario of the original distribution (41.3%). With the game theory you also live to monitor the system and trade another day while with the regular case you’re out for good. The results for the equity curve averaging method are also similar.

–

–

What this means is that the advanced money management techniques we have described are insurance against a worse than expected statistical scenario, ensuring that you preserve your equity if things turn sour. The price to pay for this insurance is a significant reduction in the AAR to drawdown ratio of the strategy you are trading if it in fact turns out to be as good as you expect. As with all insurance policies we need to think about the risk we are taking and whether it is worth it or not to insure our account equity against statistically unfavourable scenarios. You will most likely regret using this MM if everything goes well – as you would regret paying for a pricey earthquake home insurance when there are no disasters – but you will be very happy you purchased it if the trading system you’re using becomes much worse than expected. Atbara Obviously this shows us that there is a price to pay for drawdown reductions under worse than expected cases as there is no free lunch.

Another interesting case is when the money management seeks to make trade/no-trade predictions based on historical trade correlations (what neural network MM attempts to do) but then the problems we run into are related to whether there are or aren’t any correlations (more on this on a future post). All the above MM techniques are currently being implement on the latest F4 framework version – out during the next 2 weeks – so our community will have the choice of using these techniques going forward. The above mentioned techniques are already implemented within our Monte Carlo simulator software. If you would like to learn more about algorithmic trading and money management please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach towards automated trading in general . I hope you enjoyed this article ! :o)

Hi,

Thankyou for sharing your experiences on the web.

I’m keen to pick up a new skill, which is programming EA and learning programming on excel.

I’m wondering if you could point me to a direction so that I can start learning. I have also subscribed to your blog. Thank you once again :)

Hi Daniel,

Thank you very much long awaited result of game theory simulation. I think this will definitely improve long term survivability as profitability is about 80% money management.

I think this tool is much better for protecting against seasonality characteristics of trading strategy than completely stoping trading at particular months.

btw, from results you can see, that game theory mm is still too slow to realize, that strategy stopped working as worst case consective losses decreased only by 3 from 21 to 18.

Regards.

Hi Moodyman,

Thank you for your post :o) You need to remember that game theory bases its trade/no-trade decision on a random number roll. This means that the worst-case scenario for game theory – if the strategy works as expected – is very close to the worst case for the regular system because in the game theory worst case the random number rolls make us trade, even on very low probabilities. This is the reason why the consecutive losses are almost the same between the two money management strategies. It is not a matter of game theory being “slow” but a consequence of having a very unfavourable randomly based outcome in 100K simulations (it has nothing to do with how “fast or slow” game theory acts). I would suggest you to review the fundamentals behind game theory (rewatch the videos available at Asirikuy if you are a member) to get a better idea of why these results appear in this way.

I also do not think that this a substitute for avoiding trading on statistically relevant seasonality. If you know that a strategy has a statistically significant chance of being unprofitable during a certain period it is a “waste of information” to trade within this period in any case. The important thing here is establishing seasonality based on strong statistical grounds so that you are not fooled into avoiding trading during periods that aren’t showing this effect. Thanks again for posting :o)

Best Regards,

Daniel

I guess the big strenght of Game Theory is in the management of a whole portfolio, more than single systems. Anyway, as always very nice results.

Best.