During the last few years many Forex brokers have given investors the option to day trade “stocks” through the use of contracts for difference a.k.a CFDs. The offer seems very appealing, you get to use the leverage and software used in FX trading (which is a huge repository by the way) with the advantage that your minimal capital requirement drops from 25,000 USD to day trade US stocks, to about 10 USD on some Forex brokers. You can take trades with up to 1:50 (sometimes 1:200) leverage as well, something you would never dream of doing when trading real stocks in the usual manner. However it is important to realize that contracts for difference (CFDs) are not stocks and that trading them as if they were real stocks carries a huge risk. Through the rest of this post I want to explain why this is the case and in which ways you can actually take advantage of CFDs to compliment your actual trading (if you’re still interested after reading about their disadvantages).

–

–

Let us start by defining what a real stock is. A real stock represents a real stake within a given company, it constitutes a form of ownership. It means that you will benefit from both the company’s positive value creation (its growth through time) as well as any eventual profit that the company chooses to distribute to shareholders (through dividends). As a group, stocks benefit from these two fundamental factors: long term positive bias (a consequence of this being a positive sum game) and dividend payments. This means that if you own something like the S&P500 (which you can easily do through an ETF like the SPY), your long term growth prospects are positive and you will – in addition – receive dividend payments on a certain time basis. When you day trade stocks, you still enjoy these two benefits, only that you can enter/exit positions on an intra-day basis (on the same day).

When you talk about CFDs, you’re talking about an entirely different thing. Contracts for difference are derivatives where you are promised to be paid the difference between the price of an asset when you purchased the contract and when you want to sell it. In essence the contract stipulates that if you buy a stock at 1.5 and then you exit it at 1.6 you are paid 0.1 for whatever lot quantity you chose. Why is this any different from buying a stock at 1.5 and selling it at 1.6 ? Aside the trading costs – which can in some cases be lower or CFDs, as sometimes only the spread is paid – there doesn’t seem to be anything wrong. Well, think again ;o)

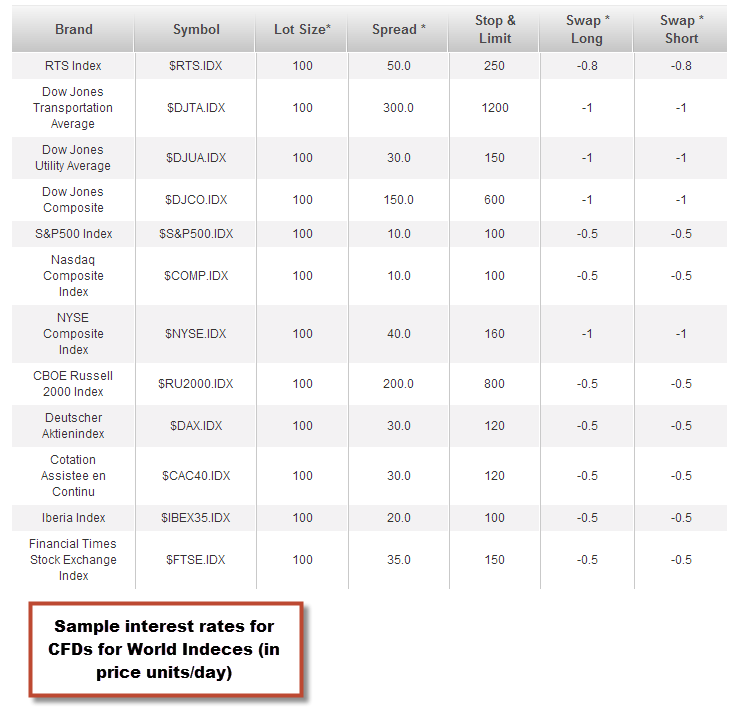

In CFDs, there is a counter-party to your contract – the one who makes the deal to pay you the difference and they are aware that they are at a disadvantage due to the fundamental positive bias and dividend payments on real stocks. This means that you could buy the S&P500 CFD with leverage and you could profit from the long term tendency of the index to move up while the contract issuer would absorb all the loss. In essence a CFD contract issuer is not willing to let this be a positive sum game for you, so they need to turn it into a negative sum game for the trade. How do they do this? Well, they charge you interest on a daily basis that largely eliminates the long term bias advantage (almost completely in some cases). If you held a CFD for the S&P 500 the index could go up and you would still lose money because your CFD contract requires interest payments that are aimed at reducing any long term positive bias by a large margin. It is therefore extremely important that you hold a CFD only between the open/close of a day (for longs) because failing to do so (having a stock CFD trade opened for longer) will lead to large and negative interest charges that will eat significantly through your profitability. http://fhaloanmichigan.org/fha-loan-in-roseville-mi/ Most brokers also charge you triple swap if you keep a CFD position across the week-end!

–

–

Could you just buy on open and sell on close to benefit from the long term bias? Actually you cannot because gaps are incredibly important for stock trading. As a matter of fact, most of the positive bias in the S&P500 isn’t generated during trading hours but it’s generated during gaps that happen across trading sessions. If you look at the skewness and mean of the SPY (as we did have done within our Using R in Algorithmic trading series) you will notice that the values for the 100*(Close[n]-Close[n-1])/Close[n-1] returns are 0.1257 and 0.034 while for the 100*(Close[n]-Open[n])/Open[n] returns are -0.00011 and -0.00071. When you remove gaps from stock trading you are faced with an almost neutral (slightly negative) scenario. This means that you will not be able to make any money by opening/closing trades just to be in during the trading session.

The above however doesn’t mean that CFDs are useless, it just means that they should not be viewed as real stocks are. In essence CFDs eliminate all the positive sum game nature of stock trading and you’re faced what in essence is a negative sum game, all alike Forex trading. In addition stocks – without their attractive positive bias and dividends – are terribly hard to trade instruments with a very large degree of kurtosis (>7 in most cases, even when not considering gaps) making profitable trading from long term edges a really difficult endeavor. However, if you found an intra-day system you would like to trade, you would benefit from trading CFDs Vs real stocks, because on real stocks you would lack large leverage, your capital requirements would be higher and you would also probably pay higher commissions. The advantage goes to CFD trading whenever you want to attempt to exploit trading edges that do not require trade holding after a day’s close. However it’s worth considering that CFD trading without commissions also carries a larger spread when compared to real stock trading. http://davidpisarra.com/wp-content/plugins/woocommerce-upload-files/js/wcuf-admin-menu.js Do you use CFDs in your trading through your FX broker ? What are your experiences and uses for these instruments ? Leave a comment :o)

In my view, the problem in the end is that profitable CFD trading requires a long term statistical edge derived solely from market timing without the benefit of the positive sum game, a difficult thing to achieve especially when involving high kurtosis instruments. Kantu can be used as a first approach to attempt to develop such edges. If you want to learn more about market characteristics and how you too can develop your own historically profitable trading strategies please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach towards automated trading in general . I hope you enjoyed this article ! :o)

Hi Daniel, congratulations for your interesting articles!

A few years ago came the news of the famous “Dodd-Frank Wall Street Reform Act” and one of the probable consequences would be the prohibition of forex trading and other instruments for retail traders, in your opinion, Daniel, would be possible this kind of act in the near future that destroying the hopes of those who want to start business with home trading?

Thank you and keep up the good work!

Hi Carmine,

Thanks for your post :o) I don’t think that the Dodd-Frank act would want to “remove” retail traders from the FX game. There are several companies that would heavily lobby against it (such as FXCM) but – as you might know – the government has indeed sought to remove the exposure of the retail market to high risk, by doing things such as heavily reducing leverage. Trading companies can be a powerful lobby, so I doubt they would go down without a fight. Thanks again for commenting and reading my blog :o)

Best Regards,

Daniel

Hi Daniel,

You wrote that:

” When you remove gaps from stock trading you are faced with an almost neutral (slightly negative) scenario. This means that you will not be able to make any money by opening/closing trades just to be in during the trading session.”

This is true if you take only long or only short positions. It means that the distribution is centered at 0 with a negative skew. It says nothing about systems with timed entries and selectively going long or short. I do not agree with this kind of mixing of statistics with trading. The fact that it is difficult to find successfultrading systems should not be attributed to average statistics but to a lack of understanding of how this can be done.

Note: Skewness can be positive but the annualized return can be negative. Also, skewness of large cap stocks is negative but returns are positive. I see some statistics confusion lately in your writings. If you develop trading systems you should not care where the fat tails lie but whether your system capture the gains. The statistics you refer to should matter only to longer-term investors or long-only/short-only traders.

Hi Bob,

Thanks for your post :o) Yes, I agree with you (sorry if there is any confusion in my writing). I was trying to make the point – as you say – that if you’re an investor this type of instruments won’t work with you because there is no long term fundamental bias you can take advantage of. The only thing I wanted to point out is that to be successful trading these instruments you need to know how to gain a long term edge, which cannot come from the natural bias of the underlying stocks (in the case of CFDs), meaning that – as you also say – you need to find a system with timed entries that has an edge. Regarding the quote you mention, I was referring only to the fact that you cannot make money simply by going long on market open and closing on market close everyday, trying to avoid the long term interest of CFDs.

Regarding Kurtosis, it’s been my experience that developing systems for high Kurtosis instruments is harder. I agree that if you have a model that properly accounts for the fat tails you can potentially take advantage of them but in my experience these fat tails – especially on FX instruments – are caused mainly by events that are unpredictable (such as central bank interventions for example). However, I take the point you make that it can be done, I’m not saying it cannot merely that I’ve found it more difficult (sorry if it comes across differently).

I’ll try to be more careful framing these issues on future articles. Thanks again for commenting,

Best Regards,

Daniel

PS: Always feel free to post any short-comings or problems in my articles, it always helps me to become a better trader and writer :o)

Thanks Daniel but again I find something confusing here. Long term investors do not buy on the open and sell on the close. Actually buy and hold is equivalent to continuous buying at the close and selling at the next close without commission expenses. So I fail to see what this has to do with investors. I also fail to see what this has to do with traders. These are average statistics and reveal little about the potential of non-ergodic systems. Note that all trading systems are non-ergodic but average statistics are ergodic. These are two different things that cannot be mixed.

“you need to find a system with timed entries that has an edge.”

I agree. this is the task at hand and it is difficult because as you wrote in the past markets constantly change.

Regarding skewness: it says little when looked upon isolated from other moments. No useful conclusions can be drawn from it. Thanks

Hi Bob,

Thanks for the reply :o) I know that the buy-and-hold assumes a permanent long position. What I meant is that if you’re an investor seeking to profit from the buy-and-hold in stocks using CFDs, you would want to avoid the interest charged on market close so a potential strategy would be to attempt to go long on open and then exit on the close so that you would be long but never be charged interest. I wanted to show that this cannot work because in the long term the movement during the day has a neutral average if you cannot profit from the day-to-day gaps. Long story short, I wanted to show that CFDs are not good instruments for buy-and-hold type strategies.

About skewness, I agree that it says little without further context – especially regarding the development of systems with timed entries – I will strive to give these values more context in the future to reach more useful conclusions. Your posts are very useful, thanks again for commenting :o)

Best Regards,

Daniel