During the past couple of years (2012 and 2013) we have seen some significant changes in the market that have made many previously profitable systematic inefficiencies, unprofitable. During the years 2008-2011 (till about mid 2011) profit was seemingly easy to achieve using statistically sound historically developed algorithmic strategies in FX trading, a good reason why I was able to obtain some significant benefits from trading such strategies during this market period. However many (thankfully not all) of the strategies we developed through this time have either failed or entered long and sometimes heavy drawdown periods, despite their apparently sound statistical character (long term historical testing, etc). Is there some systematic problem that we are facing right now? Is it here to stay? On this blog post I want to go a bit deeper into what has been going on within the past few years and what I think we can expect going forward.

It is no secret that algorithmic trading had some “golden years” between 2008-2011. Through this period – most notably due to the high directional volatility of the financial crisis – systems based on a wide variety of market characteristics were able to obtain high amounts of profit, with an almost completely negative correlation with equity markets. Among the high-performers found during this period, trend followers were perhaps the most impressive, with some systems achieving returns of more than 100% of capital within this period, with little drawdown whatsoever. During these years everyone trading algorithms was making a killing. Then, change happened.

–

–

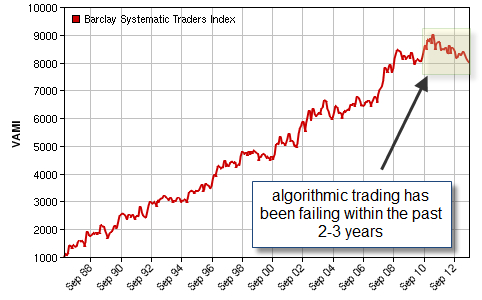

This phenomena is not simply something I’ve experienced as a retail trader, it has also been experienced widely by hedge funds, other retail traders and banks. For example this article highlights how money has been flowing out of quantitative investment ventures due to their inability to match performance expectations. It is no mystery that during the past few years most systematic traders have under-performed, even those with a lot of human resources (those with the Math and Physics PhDs) and lots of cash to spend. Proof of this is the Barclay’s systematic trader index – picture above – which has been substantially under-performing during the past 3 years. As you can see this index had never faced two consecutive losing years and now it has faced three losing years in a row, all of them facing loses in the 2-4% range. As you can see the experience of the Barclay systematic trader index also closely matches mine, a very good 2008-2010 period, followed by much worse results from 2011 till 2013. You see a steady “bleeding” of equity during this market period.

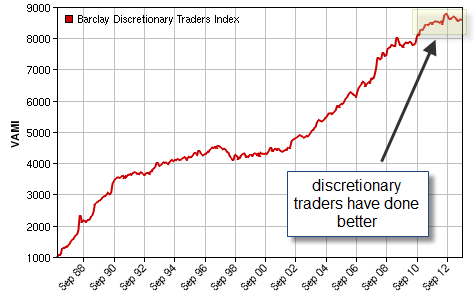

Contrary to this, discretionary traders have been able to maintain their edge quite well – despite changes in market conditions – with their last three years being profitable and only their last year being slightly in the red to date. Therefore systematic traders are doing something wrong, while discretionary traders seem to be successfully adapting to whatever change is currently going on. Why is this the case ? Why have human traders been able to out-perform algorithms during the past several years, what is happening that has been so hard – for even the most adept human system designers – to generate profit in an algorithmic manner?

–

–

The answer seems to be simple and at the same time incredibly complex: fundamental influence and uncertainty. Algorithmic trading systems are all designed with the idea that some historical assumption will continue to be true in the future. This assumption can be that price tends to break at a certain hour, that momentum created in one direction leads to continuations, that two instruments are co-integrated, etc. When these assumptions break, the algorithms fail because they have no way to know that under current market conditions their assumptions are no longer valid. This “breaking up” of algorithms means that we usually need to take loses to realize that something has changed – to remove or modify our strategy – and this makes us invariably less reactive than human traders. http://annedickson.co.uk/awiyor/ The strength of algorithmic trading, it’s high capacity to exploit structural characteristics, becomes its weakness when the underlying structure changes.

When central bankers are intervening in the market (read Fed QE, BOJ easing, SNB floor, etc) and there are new fundamental scenarios (EU sovereign debt crisis, US congress indecision, etc) the market structure becomes uncertain and some underlying players change the way in which they trade. This in essence creates the ideal conditions for a failure of algorithmic trading systems. You think you’re trading some valid causal correlation in the market, but that aspect was only valid under some different market conditions. Systems cannot simply foresee these changes, while human traders can in someway anticipate them because they have much broader context (they are not limited by data but can also have a “feel” of current market conditions (fear, despair, uncertainty, etc), which systems lack). buy cenforce 150 mg with credit card This teaches us that when markets are heavily influenced in non-systematic ways by changing fundamental events, human traders play better (at least up until now).

–

–

Does this mean that mechanical trading seeking alpha is doomed? I think it’s not, but it means that systematic trading will need to endure this period (and others like it in the future) before another positive period comes our way (it’s no holy grail). Systematic trading performs really well when the markets are facing some defined direction – being bullish (1990s bull market) or bearish (financial crisis) – as long as the market has a clear idea of where it’s going. The financial crisis provided systematic traders with very positive earnings that serve as a “cushion” for the following years of poor results but systematic trading is likely to under-perform as a whole until we get some “clear direction”. My bet is that systematic trading will have a new and good run when we start to see a true recovery around the world picking up steam and the influence of central banker talk (such as tapering by the Federal Reserve) becomes much less influential.

In the meantime, there are some strategies that haven’t failed within this period and have been able to maintain some measure of positive performance. In my experience the key under current market conditions is to attempt to trade with low frequency – limit the possibility of large numbers of consecutive losing trades as conditions change to something you’re not prepared for – and make sure that the systems you trade are based on robust analysis/trading techniques. Something fundamentally important, make sure you continuously evaluate strategies and discard them whenever they stray from their development statistics. It is specially important to also derive statistical limits for the trade number you have and not for very large number of trades (it’s not the same to reach a 10% drawdown in 5 trades than to reach it in 50 trades!). This will allow you to switch off a system quickly knowing that the chance of having a “false positive” (switching off a working system) is low. Under current market conditions, it pays more to be safe than sorry.

If you would like to learn more about systematic trading in the FX market and how you too can build your own systems using our professional framework please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach towards automated trading in general . I hope you enjoyed this article ! :o)

[…] Here is another article… […]

Hi Daniel,

a few months ago I wrote a post on asirikuy forum whose title was “The infinite power of central banks”.

I wanted to pinpoint that no matter how our systems are developed and tested over historical data if institutional entities enter the game with such a frequency and weight.

You answered that my observation was anedoctal. Of course I did it as a human being or if you prefer with the mindset of a discretionary trader.

Now that anedoctal observation is turning out to be a truth that is crashing some our systems and giving hard times to others.

For a while within asirikuy you started to develop game theory algos, that could work as a fail-safe device (i.e. preventing systems from taking trades in such periods), but that development was stopped for some reasons I don’t remember.

Best,

Rodolfo

Hi Rodolfo,

Thanks for posting :o) Of course, central bank intervention can be both negative or positive, depending on how it aligns with the overall market expectations. Historically this wasn’t problematic – it more often than not generated further momentum in the overall market direction – but it is true that during the past two years the influence of central banks has been disruptive, in the sense that FX instruments have behaved fairly different than in the past 25 years (momentum behavior has changed quite dramatically).

About game theory, the issue is that Monte Carlo game theory simulations showed that you would need to compromise your best case AAR/MaxDD ratio by a factor of 3-5 if you wanted to pay this insurance. This means that if things turned out to work as you expected them to, you would have very heavy regret (you would miss a ton of potential profit but your drawdown would still have been similar). Of course, if things turned out badly you would exit much sooner and you would be very happy about that. Game theory is a very good idea to protect you from system failure, but there is a big price to pay for this if things happen to work out as planned. In the end the high compromise in the expected profitability is something most traders are not willing to accept.

Thanks again for posting :o)

Best Regards,

Daniel

Hi Daniel,

I would recommend you to have a look to this model that finally brings something new to the table in the systematic fx world.

http://ssrn.com/abstract=2419243

Contrary to the latest awful results of classic momentum or carry models (no matter how sophisticated they are), this model beats them all.

Best,

J.