About a month ago I wrote a post about our system execution in Asirikuy after more than a million trades and how this execution compared with the expected entries and exits from back-testing. From this analysis it was evident that our execution was overall worse in live trading when compared with our simulations, meaning that our simulations were overly optimistic in terms of the expected profit we were supposed to get. Due to these issues we decided to take steps to solve this problem by increasing the spread in the GBPJPY and the USDCHF in order to have more realistic simulations and end up with live trading execution that would – if anything – be more favorable than what we expected from backtesting. Today I want to tell you how things have changed after one month of using higher spread costs in our simulations.

–

–

Increasing our spread costs in simulations was not a very easy decision to make as we knew this would make many of our strategies worse in back-testing, forcing us to leave them behind. As a matter of fact the increase in spread costs in the GBPJPY from 5 to 8 pips caused us to lose around 400 trading systems for this symbol, since they were no longer able to meet our profitability requirements after exposed to the higher spread level. On the USDCHF – were we increased from 3 to 5 pips – we also lost some systems although they were far fewer, mostly because we have less systems for this pair compared to the GBPJPY. After making these changes we saw some immediately positive results, becoming more positive as trading continued through the month.

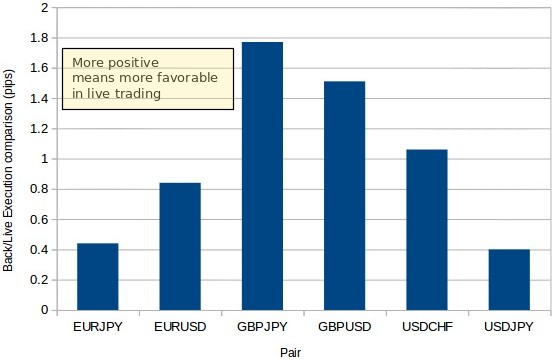

The above image shows you the current back-testing Vs live trading difference for our strategies. This measures the average of the sum of the difference in entries/exits – accounting for trade direction – such that we get a positive number if live trading is more favorable and a negative number if back-testing is more favorable. As you can see above we are now at a point where every symbol has a net favorable execution and the GBPJPY has gone from around -8 pips to now being close to +1.8 pips. This means that we went from executing on average 8 pips worse to now executing 1.8 pips better than what the simulations are predicting. The difference in the USDCHF is also very significant, large enough to take the pair into positive execution territory as well.

–

–

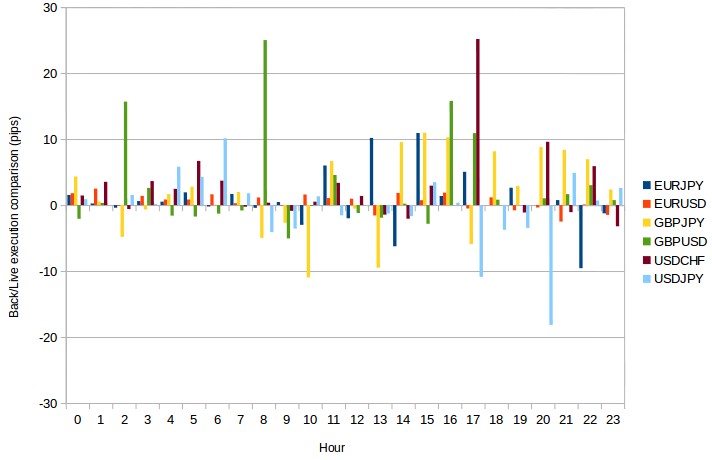

It is also worth noting that the difference has been caused by a few factors. The increase in the spread made systems that continued to trade behave more pessimistically in back-testing but it also removed systems that performed significantly worse when exposed to a higher spread. This meant that trading after these changes was both through more pessimistic simulations and using a far smaller number of spread sensitive strategies. This also caused a dramatic difference in the back/live comparisons on a per hour basis as you can see in the second image in this post. While previously the GBPJPY traded unfavorably under most hours we now have a fewer number of unfavorable hours now coupled with a few hours where we execute on average considerably much better than in the simulations. However some of these effects might also be due to recent weeks were significantly favorable slippage has affected some strategies. If you compare this graph with the one on the previous post please note that the color conventions are different in both cases.

Our simulation costs have also consistently moved into more favorable territory since these changes were carried out. This points out that the systems that were eliminated were significantly negative contributors to trading costs since once we stopped using them our live trading execution started to increased over the weeks, as the contributions from the trading of these systems – which are now not trading – have diminished and only systems that aren’t prone to be too spread dependent remain. We expect our average trading cost to converge at some point to a value that should allow us to assess whether we have under or over shot our spread correction. However we expect to always have at least a slightly more favorable execution in live trading Vs back-testing to ensure that our simulations aren’t overly optimistic but rather slightly pessimistic.

–

–

If you would like to learn more about our live trading and how you too can trade using hundreds of trading strategies please consider joining Asirikuy.com, a website filled with educational videos, trading systems, development and a sound, honest and transparent approach towards automated trading.strategies.